If you’re reading this, I’m going to guess something about you.

You’re not 18. You’re not coming straight out of high school with your parents’ help. You’re an adult — maybe a single mom, maybe new to Canada, maybe someone who’s been working for years and finally decided to go back to school. And you’ve heard OSAP can help pay for it.

But here’s the thing you’re probably feeling right now: the application looks intimidating. There are forms, tax documents, deadlines, and acronyms you’ve never heard of. And somewhere in the back of your mind, a voice is asking: what if I mess this up and get nothing?

I get it. Over the past few years, I’ve helped more than 200 adults apply for OSAP — single parents on their own with two kids, newcomers who landed in Ontario six months ago with no credit history, people who were convinced they’d never qualify because of a past loan default or a bankruptcy. I’ve seen the exact mistakes that get applications flagged or rejected, the grants people miss because nobody told them they existed, and the panic that sets in when a rejection letter arrives three weeks before tuition is due.

This guide is everything I’ve learned from those experiences. These are the seven mistakes I see over and over again — plus one bonus trap almost nobody talks about — and exactly how to avoid each one.

Table of Contents

- The 2026 OSAP Changes You Need to Know About First

- Mistake #1: Reporting the Wrong Income on Your Application

- Mistake #2: Forgetting the Signature and Declaration Pages

- Mistake #3: Not Knowing You Can Decline the Loan

- Mistake #4: Dropping Below the 60% Course Load Threshold

- Mistake #5: Missing the MSFAA (The Agreement on a Completely Different Website)

- Mistake #6: Applying With a Past Default or Overpayment You Forgot About

- Mistake #7: Not Classifying Yourself Correctly (Single Parents, This One Is for You)

- Bonus: The OSAP Affidavit Trap Nobody Warns You About

- FAQ: Your Most Pressing OSAP Questions, Answered

- Final Thoughts: Why I Do This Work — And How I Can Help

The 2026 OSAP Changes You Need to Know About First

Before we get into the mistakes, there’s something happening right now that you can’t afford to ignore.

In February 2026, the Ontario government announced major changes to OSAP. The grant maximum — the “free money” portion you never have to pay back — is being slashed from 85% of your funding package to just 25%, effective Fall 2026.

What does that mean in real numbers? If you would have received $6,000 in provincial aid under the old system, about $5,100 of that was grants. Under the new system, only about $1,500 will be grants. The rest becomes a loan you have to repay — roughly $3,600 more in debt per year, or over $14,000 across a four-year program.

Students across Ontario are describing these changes as “heartbreaking” and say they feel “discouraged” about even applying, according to CBC News. CTV Windsor reported students saying they’ve been “blindsided” — especially those mid-degree who budgeted under the old rules and now face a funding gap they never planned for.

My honest take: this makes it more important than ever to get your application right the first time. Every dollar of grant funding you qualify for matters more when the grants are smaller to begin with. Every mistake that delays or reduces your funding stings harder. And every strategy to maximize what you get — which I’ll share below — is worth twice what it was last year.

Let’s make sure you don’t leave anything on the table.

Mistake #1: Reporting the Wrong Income on Your Application

This is the single most common mistake I see, and it’s an expensive one.

OSAP doesn’t want your best guess at what you earned. It doesn’t want the number on your most recent pay stub. It wants Line 15000 from your CRA Notice of Assessment — your net income, not your gross income.

I’ll never forget a single mother I worked with last year. She entered her gross employment income — what her employer reported on her T4 — because that’s what she thought “income” meant. Her application was flagged within days. The OSAP system cross-references everything with the CRA, and when the numbers don’t match, your file gets frozen. She had to resubmit and wait another three weeks — with tuition due and childcare to arrange. The stress was written all over her face.

The fix: Open your CRA My Account before you even start the OSAP application. Pull your Notice of Assessment for the tax year OSAP is asking for. Look at Line 15000. That’s your number. If you’re married or common-law, pull your spouse’s too. Never estimate. If your income dropped significantly since that tax return — maybe you lost a job or went on maternity leave — don’t just report different numbers. File an OSAP review through your school’s financial aid office with proof of the change. That route exists for a reason, and most people don’t know about it.

Mistake #2: Forgetting the Signature and Declaration Pages

This one genuinely frustrates me because it’s so avoidable, yet it trips up so many people.

You fill out the entire online application. You hit submit. The screen says “submitted,” and you breathe a sigh of relief. Then you wait. And wait. A week goes by. Two weeks. Nothing.

What the OSAP portal doesn’t make obvious — and in my opinion, this is a design failure — is that submitting the online form is only step one. You also need to print, physically sign, scan, and upload the declaration and signature pages. Without those signed documents, your application sits in limbo. OSAP won’t process it. They won’t send you an email reminder about it either. You have to log into your OSAP account, open the message center, and look for document requests yourself.

I’ve had clients call me three weeks after submitting, wondering why their funding estimate hadn’t appeared. Every single time, it was the signature pages.

The fix: The moment you click submit on the online form, print the signature pages. Sign them. Scan them clearly — a clean scan, not a blurry phone photo from a dark room. Upload them immediately. Then set a weekly calendar reminder to check your OSAP message center. Treat it like checking your bank account. Missing document requests live there, and they have strict deadlines you can’t afford to miss.

Mistake #3: Not Knowing You Can Decline the Loan

This isn’t exactly a mistake that gets you rejected. It’s a mistake that costs you years of unnecessary debt — and in my experience, it’s one of the most poorly communicated aspects of the entire OSAP system.

When OSAP calculates your funding, it gives you a total package: some grants, some loans. What most people don’t realize — and what the acceptance screen certainly doesn’t advertise — is that you can accept the grants and decline the loans.

You are never required to take the loan portion of your OSAP funding.

I once sat across from a client who had taken out $7,000 in loans over two semesters. When I asked why, she said, “I didn’t know I could say no to part of it. I thought it was all or nothing.” She had $7,000 in debt she didn’t need, all because the system never made the distinction clear.

This matters more now than ever. With the 2026 cuts dropping the grant portion to 25% of your package, you need to know exactly which part is free and which part you’ll be paying back with interest for the next several years. Before you accept any OSAP funding, look at the breakdown. Identify what’s a grant and what’s a loan. Ask yourself if you truly need the loan. If you don’t, decline it. That money will still be there if your situation changes and you need to borrow later.

Mistake #4: Dropping Below the 60% Course Load Threshold

A client of mine — a working mother of one — called me in a panic last fall. She had enrolled in what she thought was a full course load at her college. Two weeks into the semester, one course was clashing with her child’s daycare pickup. She couldn’t make the schedule work, so she dropped it. Simple fix, right?

A month later, OSAP sent her a reassessment letter. Nearly $2,800 in grants — money she had already budgeted and spent on textbooks and transportation — was being converted to loans. She now owed that amount back, and her remaining funding for the semester was slashed.

What happened? OSAP requires you to maintain at least a 60% course load for full-time funding. When she dropped one course, she fell to 50%. The system automatically reassessed her file, and the grants were clawed back.

Here’s what makes this particularly cruel: different schools calculate course load percentages differently. What counts as 60% at one college might be 40% or 70% at another, depending on how they weight their courses. You cannot guess this number.

The fix: Before you drop anything, ask your financial aid office for your exact course load percentage. If dropping a course would push you below 60%, explore alternatives first — sometimes swapping to a different course with a better schedule keeps you above the line. If you genuinely need to drop below 60% due to medical reasons or a family emergency, file for an exceptional circumstance review immediately. Don’t wait for the reassessment letter. By then, it’s already too late.

Mistake #5: Missing the MSFAA (The Agreement on a Completely Different Website)

This is the mistake that makes people feel genuinely stupid, and I hate that, because it is absolutely not their fault.

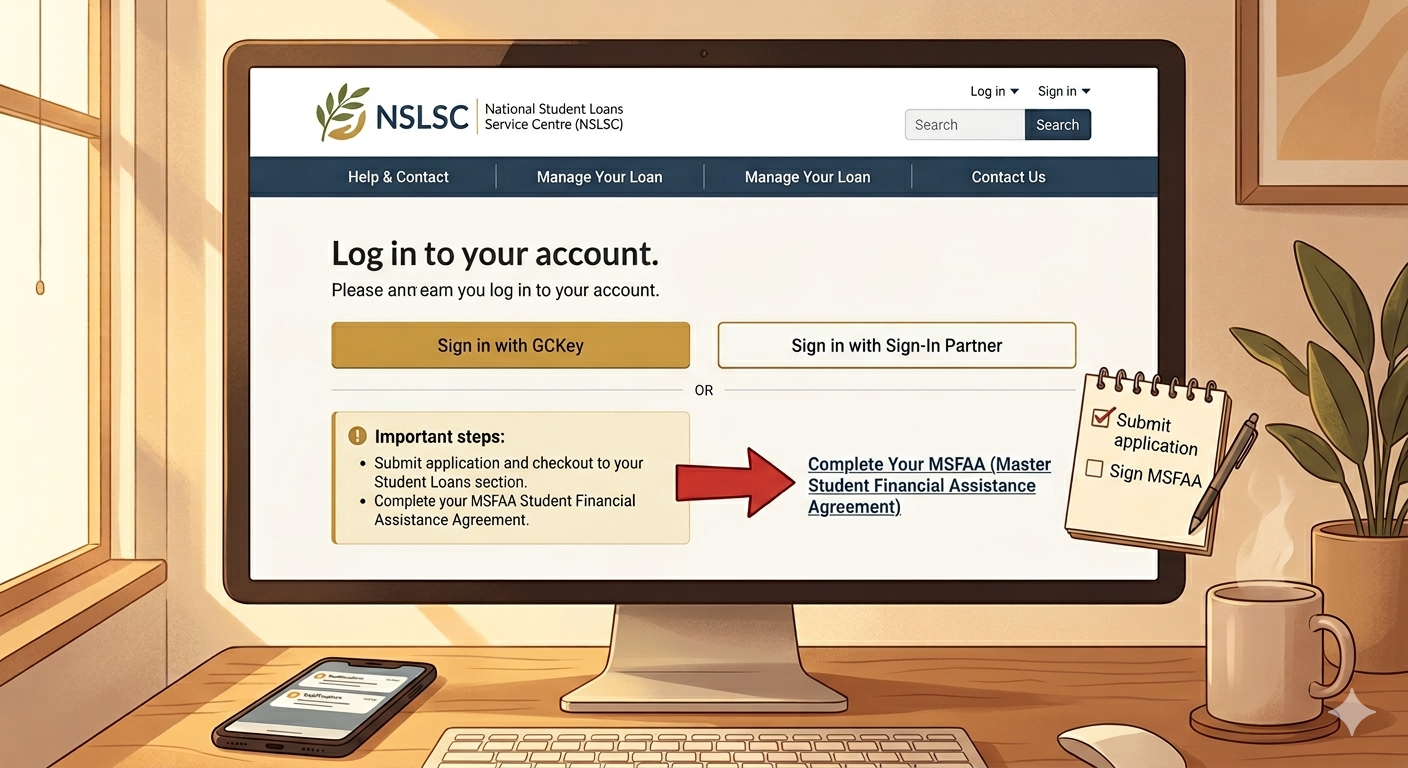

The MSFAA — Master Student Financial Assistance Agreement — is a separate multi-year contract you sign with the National Student Loans Service Centre. It is not on the OSAP website. It is on the NSLSC website. These are two completely different government portals, with two different logins, and nobody explicitly tells you this when you’re applying for the first time.

I can’t count how many first-time applicants have called me saying, “I did everything — the application, the signatures, the documents — and my funding still hasn’t come.” I ask about the MSFAA, and there’s a long pause, followed by some version of “my what?”

The Ontario Ombudsman has even documented cases of OSAP processing failures that delayed students’ funding through no fault of their own. The system has genuine gaps. When you hit one of them, it’s easy to blame yourself. Don’t.

The fix: After your OSAP application is processed, you’ll get instructions to complete the MSFAA through the NSLSC. Do it immediately — same day if possible. If you’ve received OSAP in a previous year, your MSFAA might still be active, but log in and confirm. Keep your NSLSC login somewhere permanent — you’ll need it for years, not just for this application but for checking your loan balance, applying for repayment assistance, and updating your information down the road.

Mistake #6: Applying With a Past Default or Overpayment You Forgot About

This one is the hardest to write about, because the people it affects are often the ones who need OSAP the most.

If you have a past OSAP loan in default or collections — or an unresolved overpayment on your account — your new application will be rejected. It doesn’t matter if the loan was from eight years ago. It doesn’t matter if you thought it was resolved. OSAP checks, and the system does not give second chances without you clearing the issue first.

And here’s the part that genuinely disturbs me: there are documented cases on forums like Canada Student Debt of OSAP retroactively reassessing grants issued in the early 1990s — 15 or more years later — and demanding repayment with accumulated interest. Imagine getting a collection notice for a grant you received when your kids were toddlers, and now they’re graduating high school. The Ontario government exempted itself from statutes of limitations on these debts. They can resurface at any time.

I’ve seen what this does to people. The excitement of “I’m going back to school” turns into dread when the rejection references something from a decade ago that you barely remember. It feels like the system is punishing you for trying to improve your life.

The fix: Before you submit a new OSAP application, log into your NSLSC account and check for any outstanding loans, defaults, or overpayments. If something is there, deal with it now. Contact the NSLSC about loan rehabilitation options. Negotiate a repayment plan for old overpayments. If you filed for bankruptcy, confirm that at least seven years have passed since your discharge date. Applying blind and getting rejected doesn’t just waste an application cycle — depending on the reason, it can flag your account in ways that make future applications harder.

Mistake #7: Not Classifying Yourself Correctly (Single Parents, This One Is for You)

This is the mistake that costs people the most money, and it’s the one I find hardest to watch because the fix is so simple once you know about it.

If you’re a single parent — a mom or dad raising a child on your own — OSAP has a classification called sole-support parent. Under this classification, your weekly funding maximum jumps from $510 to $825. Your child care bursary increases from $40 to $83 per week per child. And you receive additional grant consideration because OSAP recognizes you’re supporting a family while you study.

But here’s what I see happen over and over: single parents select “single” on their application. They’re not being dishonest — they are single. They just don’t know that OSAP has a separate, significantly more generous category for parents raising kids alone.

I worked with a mother of two last year who had already submitted her application classified as “single.” When we reclassified her as a sole-support parent and updated her dependents, her grant estimate increased by more than $3,000. She had been prepared to take out loans to cover the gap. Three thousand dollars in free grant money she didn’t know she qualified for.

The fix: If you have a dependent child who lives with you at least 50% of the time, and you are unmarried, separated, divorced, or widowed, you are a sole-support parent under OSAP rules. Select that option on your application. Make sure your children are properly listed as dependents. If you’ve already submitted without this classification, contact your school’s financial aid office and request a status update — it can still be corrected.

Bonus: The OSAP Affidavit Trap Nobody Warns You About

I’m adding this as a bonus because it doesn’t fit neatly into the “7 mistakes” framework, but it trips up a specific group of people that includes a lot of my clients.

If you’re applying for OSAP and you cannot provide your parents’ financial information — because you’re estranged from them, or they live overseas and won’t cooperate, or they’ve passed away — OSAP requires a notarized affidavit. Specifically, the “Extenuating parental form”, which must be sworn before a notary public or commissioner of oaths.

This document exists because OSAP assumes, by default, that your parents will contribute to your education if you’re considered a dependent student. When that assumption doesn’t match reality, you have to prove it — in writing, under oath.

I’ve had clients who were completely stuck at this step. One was a young woman who had left an abusive home situation and had no contact with either parent. Another was a newcomer whose parents lived in a country where getting notarized documents was a bureaucratic nightmare. Both were told by well-meaning friends to “just apply anyway” — and both had their applications rejected because the parental information wasn’t provided and the affidavit wasn’t submitted.

The fix: If you’re under a certain age or haven’t been out of high school long enough to be considered independent, and you cannot get your parents’ financial details, look up the “Extenuating parental form” on the OSAP website. Get it notarized. Submit it alongside your application — not after. Many community legal clinics and some school financial aid offices offer free notary services for this exact purpose. Don’t skip this step or hope OSAP won’t notice. They will.

FAQ: Your Most Pressing OSAP Questions, Answered

“Do I qualify for OSAP if I’m a permanent resident but new to Canada?”

Yes — permanent residents are eligible for OSAP. The main hurdle is the Ontario residency requirement: 12 consecutive months living in Ontario without being a full-time post-secondary student. But the clock starts from when you established Ontario residency, and there are specific exceptions for protected persons and convention refugees. In my experience, many newcomers assume they’re ineligible and never apply — only to find out later they qualified the whole time. Don’t assume. If you’re a PR living in Ontario, check your specific timeline, and if you’re unsure, speak with a financial aid advisor who can look at your individual situation.

“I’m a single mom. Do I get more funding than a regular student?”

Yes, significantly more — but only if you select “sole-support parent” on your application. See Mistake #7 above. The difference between “single” and “sole-support parent” can be thousands of dollars in additional grants. This is not a small detail — it’s potentially the most financially impactful checkbox on your entire application.

“What’s Better Jobs Ontario, and should I apply for that instead of OSAP?”

Better Jobs Ontario (formerly called Second Career) is a separate government program that provides up to $28,000 for skills training if you’ve been laid off or are unemployed. If you lost your job and you’re looking at short-term training programs, you might actually qualify for Better Jobs Ontario — which in some cases covers costs OSAP doesn’t. The programs have different eligibility rules and different application processes. In my experience, it’s worth checking Better Jobs Ontario before committing to an OSAP application, especially if you’re unemployed and seeking career retraining rather than a traditional degree. Some people qualify for both. Some qualify for one but not the other. Don’t leave free training money on the table because you didn’t know the program existed.

“What happens if I drop a course? Will OSAP take my money back?”

Potentially, yes. If dropping a course pushes you below the 60% course load threshold, OSAP can convert your grants into loans, and you’ll owe an overpayment. Always ask your financial aid office for your exact course load percentage before dropping anything. I’ve seen too many people learn this lesson the hard way, including the client I mentioned in Mistake #4.

“I got rejected. Can I appeal?”

Yes — and in my experience, many rejections are overturned on appeal, especially when the rejection was due to a documentation error or an exceptional circumstance rather than a fundamental eligibility issue. Common grounds include medical issues, family emergencies, errors in your application data, or a significant change in your financial situation since applying. Go through your school’s financial aid office — they process reviews faster than the general OSAP helpline. Bring documentation. Don’t just explain your situation — prove it with medical notes, letters, or updated financial statements. The people reviewing your appeal don’t know you. Give them evidence, not just a story.

“When should I apply for the 2026-2027 school year?”

Now. Applications opened in May 2026. With the grant cuts taking effect for the Fall 2026 term, applying early gives you the best shot at locking in your funding before the system gets congested. OSAP officially recommends submitting at least 8-10 weeks before your program starts. In my opinion, aim for 12 weeks — the extra buffer protects you against exactly the kinds of document requests and verification delays this article was written to help you avoid.

Final Thoughts: Why I Do This Work — And How I Can Help

I want to close with something honest.

The reason I started doing this work — helping people apply for OSAP — is because I watched someone I care about go through this alone. She got rejected the first time. She fixed what she thought was wrong, applied again, and got rejected a second time. The difference between rejection and approval, it turned out, was three specific things on her application that nobody had told her to check. She eventually got approved — and she finished her program — but the process cost her months of stress and nearly made her give up on school entirely.

That experience taught me something: the OSAP system isn’t designed to be user-friendly. It’s designed to be thorough. And being thorough means there are a lot of ways for a real person with a real, complicated life to slip through the cracks.

You can absolutely apply for OSAP on your own. Everything in this guide is here to help you do exactly that. But here’s what I’ve seen after handling more than 200 of these applications: people who go it alone typically miss between $1,500 and $3,000 in grants they qualified for. About one in four get flagged for document issues that delay their funding by weeks — sometimes past their tuition deadline. And a surprising number don’t realize until long after graduation that they took on loans they didn’t need, or left grants unclaimed, or misclassified themselves in a way that cost them money.

If you’d rather have someone who does this every day handle your entire application — someone who knows the loopholes, the classifications, the appeal process, and exactly which documents trigger delays — I’ll handle your OSAP application from start to finish and get you enrolled in an OSAP-approved program at the same time.

There’s no cost to you upfront. You only pay when you’re approved, enrolled, and your funding comes through. If you don’t get funded, you owe nothing.

That’s the deal. If it sounds fair, reach out and let’s talk.